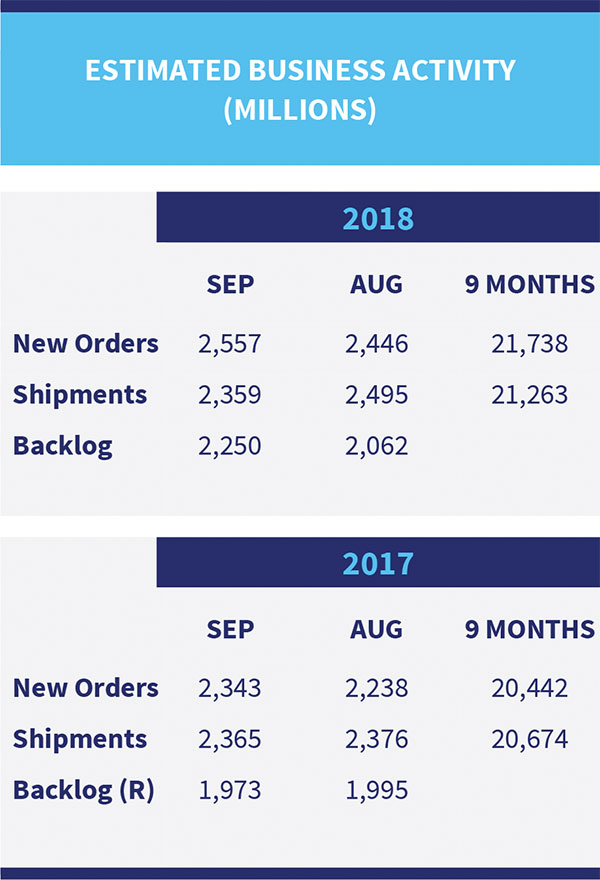

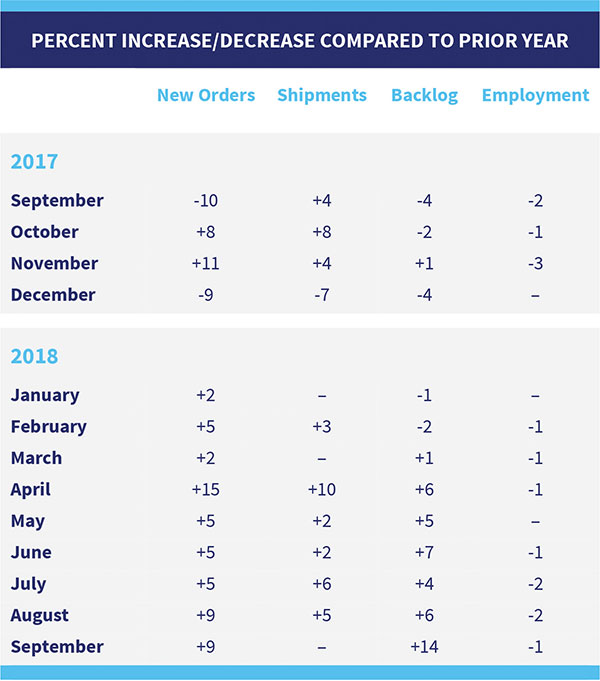

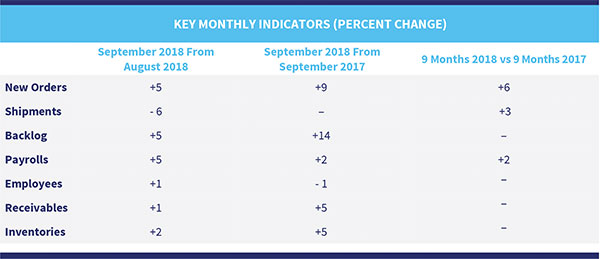

[dropcap]A[/dropcap]ccording to our latest survey of residential furniture manufacturers and distributors, new orders in September 2018 increased 9% over new orders reported in September 2017. While this increase at first appears substantial, it should be remembered that September 2017 new orders were down 10% when compared to September 2016 so the increase was really not that impressive. That said, a 9% increase in September followed a 9% increase reported in August and followed three consecutive months of 5% increases. Only 56% of the participants reported increased orders in September.

[dropcap]A[/dropcap]ccording to our latest survey of residential furniture manufacturers and distributors, new orders in September 2018 increased 9% over new orders reported in September 2017. While this increase at first appears substantial, it should be remembered that September 2017 new orders were down 10% when compared to September 2016 so the increase was really not that impressive. That said, a 9% increase in September followed a 9% increase reported in August and followed three consecutive months of 5% increases. Only 56% of the participants reported increased orders in September.

Year to date, new orders remain 6% over the same period a year ago. Last year, new orders year to date were 4% higher than September 2016. Some 76% of the participants reported year to date increases.

Shipments in September were even with September 2017 results. Shipments remained 3% ahead of 2017 year to date. Approximately 63% of the participants reported increased shipments year to date. Last year, 2017 year to date shipments were 5% ahead of the same period of 2016.

Backlogs increased 5% from August to September due to dollar orders exceeding the increase in dollar shipments. September backlogs were 14% higher than September 2017 up from a 6% increase reported last month.

Receivable levels were up 5% over September 2017 up slightly from the 3% increase in shipments year to date. Receivables are also up 1% from August 2018 in spite of a decline of 6% in shipments from August to September.

Inventories were up 5% from September 2017 and up 2% from August 2018. Overall, inventory levels appear in line with current business conditions.

The number of factory and warehouse employees continued to hold relatively steady compared to August and were down slightly from September 2017. Overall the factory warehouse payrolls seem to be in line with current conditions.

Consumer Confidence

Both surveys showed a slight decline in confidence in November, but both levels of consumer confidence remained at very high levels. The Conference Board’s report noted that the Present Situation Index improved slightly while the Expectation Index declined. For the Present Situation Index, the increase was driven by job growth while the decline in the Expectation Index related primarily to a less optimistic view of future business conditions and personal income prospects.

The University of Michigan Surveys of Consumer Sentiment Index fell slightly as well after the election. Their report noted that the drop related more to income than political party as the sentiment rose for those with incomes in the bottom third but fell more by those in the top third of income distribution.

Housing

Total existing-home sales increased in October after six straight months of declines. Single family sales were up but remained 5.3% below the sales from a year ago. Existing home sales rose in all regions of the country except in the Midwest, though all regions remained below a year ago.

Sales of new single-family houses were 8.9% below the revised September rate and were 12.0% below October 2017. Sales were down double digits in the Northeast, Midwest, and South and down 1.3% in the West.

Privately-owned housing starts in October were 1.5% above September’s estimate, but remained 2.9% below October 2017. Single family starts compared to last October were up nicely in the Northeast and West but were down in the Midwest (11.8%) and the South (10.1%).

Other

Real gross domestic product increased at an annual rate of 3.5% in the third quarter of 2018, according to the “second” estimate from the Bureau of Economic Analysis. The second quarter estimate for GDP growth was at 4.2%.

The Conference Board’s Leading Economic Index (LEI) for the U.S. increased 0.1% in October following a 0.6% increase in September and a 0.5% increase in August. Ataman Ozyildirim, Director of Economic Research and Global Research Chair at the Conference Board said, “The index still points to robust economic growth in early 2019, but the rapid pace of growth may already have peaked. While near term economic growth should remain strong, longer-term growth is likely to moderate to about 2.5% by mid to late 2019.”

The advance estimates for U.S. retail and food services sales for October 2018 as adjusted, reported an increase of 0.8% from the previous month, and 4.6% above October 2017. Total sales for August 2018 through October 2018 were up 5% from the same period a year ago. Sales at furniture and home furnishings stores in October were 1.2% ahead of October 2017. Year to date, sales at these stores were up 4.3% for the first 10 months compared to 2017.

The Consumer Price Index for all urban consumers increased 0.3% in October after rising 0.1% in September. Over the last 12 months, the all items index rose 2.5% before seasonal adjustment. Most of the increase in October was blamed on the increase in the gasoline index. The all items index rose 2.5% for the 12 months ending October, up slightly from the increase reported last month.

Total nonfarm payroll employment rose 250,000 in October. The unemployment rate remained unchanged at 3.7%.

Thoughts

The results of our September survey were positive but maybe not quite as positive as they appeared considering the comparison to a very weak September 2017. We mentioned last month that recent conversations indicated that business seemed to slow somewhat in October. At least through September, the increase in orders at 6% was positive. And with approximately 76% of our participants reporting increased orders, the improvements have been favorable for most.

After being asked by one of the participants what we were hearing more recently than the August results that we had reported last month, we conducted an informal survey of several companies, and the consensus was that business of late clearly felt slower than earlier in the year. One comment was made that retailers were having issues with getting advertising slots, either not available or cost prohibitive due to the election ads. There were certainly plenty (too many) in our neck of the woods.

The tariff issues continue to be a topic of conversation even though the 10% tariff Issue seems to have been dealt with one way or another. Many hope that the 25% level may be dealt with at the upcoming G20 Conference.

The tariff issues are a major issue for not only the furniture industry, but it also seems to be affecting many others. Certainly stock market conditions have been impacted as well, given the that time period between the end of October through Thanksgiving was not very favorable for the stock market in general.