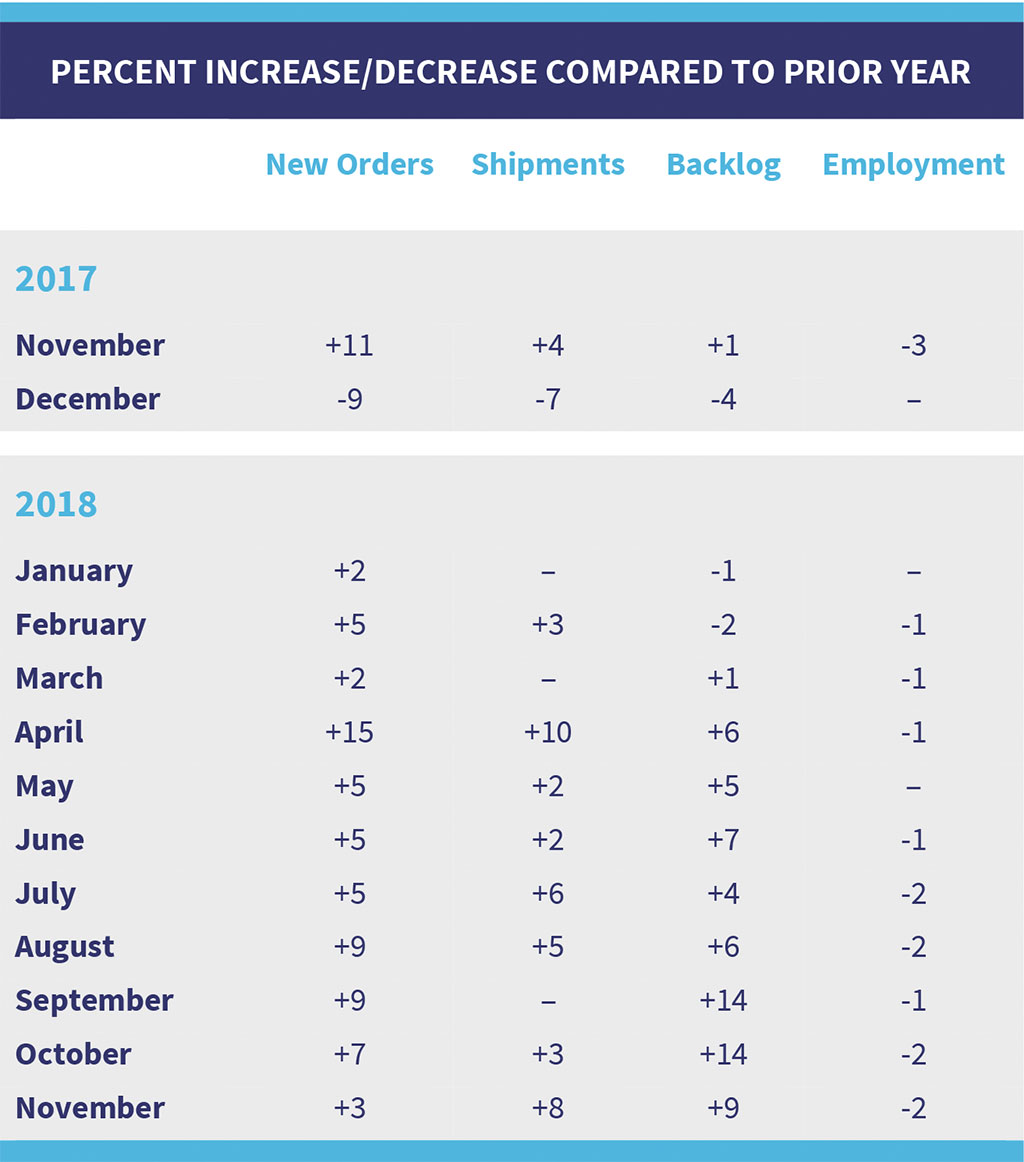

[dropcap]B[/dropcap]ased on recent conversations, we had expected to see a bit of a slowdown in new orders in the last couple of months of the year. The results of our latest survey of residential furniture manufacturers and distributors indicated a 3% increase in new orders in November compared to November 2017. This increase followed a 7% increase reported in October and 9% increases in September and August. While the 3% increase in November appeared in line with recent conversations, we looked at the results for last year’s survey and noted that new orders in November 2017 were up 11% over November 2016. So, sometimes, I think we are guilty of comparing to prior-year results without realizing that the prioryear results would have a significant impact on current year comparisons to the prior year.

New orders for the month were up for some 47% of the participants in November. Year to date, new orders remained 6% ahead of last year. In November 2017, year to date new orders were 5% ahead of the previous year. Approximately 68% of the participants reported increased orders for the year, the same as last month.

Shipments were 8% higher than November 2017 compared to a 4% increase reported in the November 2017 comparison to November 2016. We had noted that we expected shipments to start catching up some since backlog seemed to be high. Some 62% of the participants reported increased shipments for the month compared to the previous year. Year to date, shipments remained 3% ahead of last year with 68% reporting increases. Last year, year to date shipments through November were up 5%. Backlogs increased 1% in November as the dollar value of orders was higher than the dollar value of shipments. Backlogs were 9% higher than last year compared to doubledigit increases reported the last couple of months.

Receivable levels increased 7% over November 2017 and were pretty much in line with the changes in shipments. Inventories were flat compared to October levels and up 7% over November 2017. Inventory and receivable levels appeared pretty much in line with current business.

Factory and warehouse payrolls and the number of factory and warehouse employees continue to be in line with the current business conditions. The number of employees was down a bit from last year, but the total payrolls were up over the last year.

National

Note: A number of the national reports are not available at this time due to the federal government shutdown. While employees have returned to business, the reports are still not available. We hope to include these reports in next month’s publication.

Consumer Confidence

The Conference Board Consumer Confidence Index® decreased in January following a decline in December. The Present Situation Index declined only marginally, but the Expectations Index declined sharply as financial market volatility and government shutdown appears to have impacted consumers. The report noted that shock events such as the government shutdown tend to have sharp, but temporary, impacts on consumer confidence. The report noted that the month’s decline was more the result of a temporary shock than a precursor to a significant slowdown.

The University of Michigan Surveys of Consumers Index also reported a decline. This report was a bit more negative on future prospects. The major factors noted in the decline in confidence were the government shutdown and instabilities in financial markets, but also mentioned was the impact of tariffs, the global slowdown and the lack of clarity about monetary policies.

Housing

After two consecutive months of increases, existing-home sales declined in the month of December. None of the four major U.S. regions saw gains in sales activity in December. The decline was blamed to a degree on higher interest rates in 2018. With mortgage rates dropping slightly, the report indicated that they expect some revival in home sales. No results for new home sales or housing starts were available at press time.

Other

The Conference Board’s Leading Economic Index (LEI) for the U.S. declined 0.1% in December following a 0.2% increase in November and a 0.3% decline in October. The report indicated that the LEI declined slightly in December and the recent moderation in the leading index suggests that the U.S. economic growth rate may slow down this year. The leading index suggests that the economy could decelerate towards 2% growth by the end of 2019.

The Consumer Price Index for all urban consumers declined 0.1% in December on the seasonally adjusted basis after being unchanged in November. Over the last 12 months, the all items index increased 1.9% before seasonal adjustment. The index for all items less food and energy rose 2.2% over the last 12 months, the same increase as the 12 months ending in November. The food index rose 1.6% over the past year, while the energy index declined 0.3%.

Total non-farm payroll employment increased by 312,000 in December, but the unemployment rate rose to 3.9%. Job gains occurred in health care, food services and drinking places, construction, manufacturing, and retail trade.

Thoughts

The somewhat slower increase in orders in November was a little misleading. While we had heard business seemed a little slower for some, the comparison to November 2017 was a tough one as November 2017 orders were up 11% over November 2016. So, a 3% increase over the 2017 results was not all bad.

The lower Consumer Confidence reports were not surprising as they both noted that the government shutdown and stock market volatility had a major impact on lowering confidence. The existing-home sales results were a bit of a concern.

Overall, though, with orders up 6% year to date and shipments expected to follow, 2018 does appear to be a pretty decent year. Certainly, not for all, but with almost 70% reporting increases in orders, at least many had a nice year.

We will see what happens regarding the next potential shutdown. We also expect the severe weather to have some negative impact on many. Hopefully, the tariff issue will be settled. Most expect the 10% to remain, but there is still hope the 25% will not go into effect.

Stay warm for those of you affected by the brutal cold. Those of you in warm climates, go out and buy stuff.